Share

ShareHow OneClickCover Simplified Their Home Insurance Customer Journey

Risto Rossar, Insly's Founder and CEO, interviewed one of our good partners, Hutton Swinglehurst, the Founder and CEO of OneClickCover. At the end of the chat, Insly's Head of Sales, Märtin Kosk, opens up the background of our cooperation. Just a note before you jump in - for a better understanding, we labelled the conversation with their initials.

RR: OneClickCover is a very innovative MGA. As their name says, they have simplified home insurance customer journey to the extreme. Let's give the word to Hutton Swinglehurst to fill us in on what they do, and on his background.

HS: With a background in finance and investment banking, I moved into insurance about 10 years ago. Not specifically into home insurance, but I got involved with using data for risk pricing. That was the genesis of the OneClickCover idea.

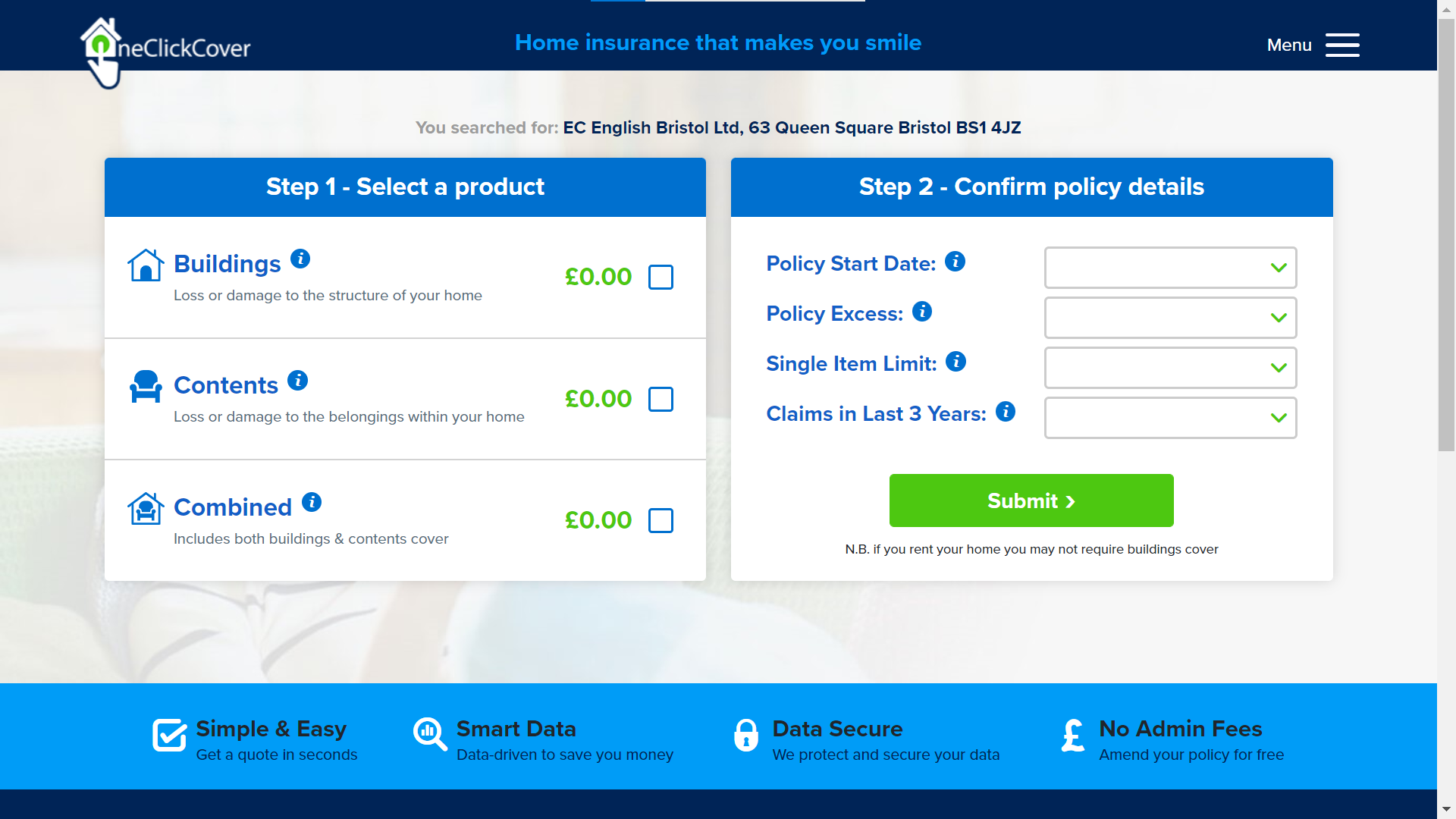

What we try to achieve is to take the rather laborious, lengthy, and confusing process of buying home insurance online in the UK and try to distill that. So, instead of answering 30 or 40 questions, we take you to the point where no questions are asked at all. We use data about the property and the occupants of the property to price the risk. This creates a full policy fulfilment ecosystem that allows the customer to buy a policy and have all of the documentation within 60 seconds.

There has to be a problem in the first place for the solution to be successful. Once we solved the issue of simplifying home insurance customer journey as much as possible, we opened up more opportunities for them. Another feature of the UK home insurance market is that customers often remain with the same insurer for a number of years. They don't shop around as much as they should, because that process is too laborious. It's too painful to spend 40 minutes of your life trying to find a quote. Whereas with our business model and process, you can get quote in a few seconds. That makes shopping around for a better deal a lot faster and simpler with us.

RR: So, the problem is there, and so is the solution, provided by you. How did you spot the problem? did you as an insurer understand that it was messy, or were you bored of filling in the forms as a customer?

HS: Actually, it was a combination of both. Firstly, it was work that I was doing in the insurance sector; I was creating a risk model that uses data for pricing flood risk. That gave exposure to the home insurance industry and to a lot of the large players. They were all going the same way, they hadn't changed the way they priced risk in any major way for many years. They were still sending out lengthy question sets for customers to fill out.

In fact, the arrival of price comparison websites (PCW) made the situation worse. PCW is about having as many insurers providing prices as you can, to make the price as low and competitive for the customer as possible. If you have 200 insurers trying to offer home insurance, they all have slightly different questions. As a result, these lists got longer and longer as more insurers were trying to offer prices. They had their own particular questions, like how far are you from a watercourse or even what percentage of your roof is flat? All of that was really painful for the customers to answer. That was combined with my personal experience of trying to get just a quote and compare it to an alternative insurer, easily. Getting a quick comparison price in a matter of seconds couldn't be done; it took over 40 minutes. That's how we arrived at the problem.

From the work I had done before, I could see that the solution lies in using data that had not been used by the insurance industry before. We took a different perspective and used partners that had expertise in providing data to property professionals about specific residential properties. That's where we started to assemble the database or the risk-pricing model that now has more than 400 different data sources contributing to it - all that to simplify home insurance customer journey.

RR: It seems simple and straightforward, but as I know, your journey hasn't been a walk in the park. What advice would you give to other entrepreneurs who would like to create a new MGA? What mountains do you need to climb?

HS: It's important to make sure that you're solving a real-life problem that people can identify with. It's not good enough just to create a product that does something differently. To be compelling, you have to have a solution to a problem that exists and is identifiable.

It's very important to find the right partners to work with, especially when you're starting out. We've been fortunate to have partners like Insly. As you are climbing the mountains, you will need to bring those partners along with you. They will need to share your vision, because difficult moments will require collaborative effort.

You need to be very patient, persistent, and not panic as an entrepreneur. Things will certainly not always go according to plan, and people may insist on a beautiful plan that marks up the future for the next few years. You need to react quickly, but without panicking. In order to analyse the situation and solve the problem, you need to think clearly and patiently.

RR: How to explain that patience to investors? Specifically, VC type of investors want really fast returns. From my experience, sometimes in the insurance business, the results are not manifesting as fast as the investors would like.

HS: You have to explain from the onset and be realistic with them about time scales- what is and what isn't achievable. Most importantly, you have to demonstrate clearly identifiable milestones that you can achieve within that time-scale. Everybody is looking for profitability, especially VCs who are also looking for their exit. Before you get to that point, you need to show that the business has moved on. Also, what has been achieved over the last couple of quarters, and how it has increased the value of your business.

A lot of people say to raise as much money as you possibly can, when you can. My tip would be to raise as little money as you possibly can, when you can. Raise what you need to get you through the next six or so months, and make sure that at the end of that period you have demonstrated some real benefits and increase in business value. That will lay good grounds for future funding. You can show what were your goals, and that you achieved them. That you uplifted the value of the business, and need more money to take it forward. We have managed to do that with OneClickCover. We have done four funding rounds and increased the value significantly every time by showing that we have hit great milestones along the way.

RR: Thank you for inspiring us and so many other entrepreneurs! Now, let's give the word to Märtin Kosk, our Head of Sales, to explain how Insly helped you on your journey.

MK: In OneClickCover's case, it all started with the data. They had access to an extensive property-risk database in the UK, on top of which they added their own underwriting guidelines. Once the idea was on paper, OneClickCover needed to build it into an online rating engine that could go through all of those 400 data points and return the price to the customer, quickly. This also had to be plugged into their website, as well as white labelled for any potential distribution partners.

Insly has a lot of experience with rating engines, and we were able to help OneClickCover with that. Though, the underwriting business is more than just a rating engine. You also need a solution for policy fulfilment - document creation, payments transaction, and transportation of documents to the customer. Ultimately, if you're an MGA, you need a policy management system where that data is stored, so you could report it back to your capacity providers. If you're looking for a solution to launch a product like OneClickCover did, make sure it has such building blocks available. Be mindful of any API capabilities which enable you to plug in additional functionalities in the future.