An insurance underwriter is a professional who is responsible for evaluating and assessing the risk of providing insurance coverage to applicants. Underwriters are typically employed by insurance companies and are responsible for determining whether or not to accept an applicant for coverage, as well as setting the terms and conditions of the coverage.

The primary role of an underwriter is to assess risk and make informed decisions about whether or not to provide insurance coverage to an applicant. This involves analysing a variety of factors, including the applicant’s personal or business history, financial standing, and any potential risk factors. Underwriters use this information to determine the level of risk associated with providing coverage to the applicant and to set the terms and conditions of the coverage.

There are several key responsibilities of an insurance underwriter, including:

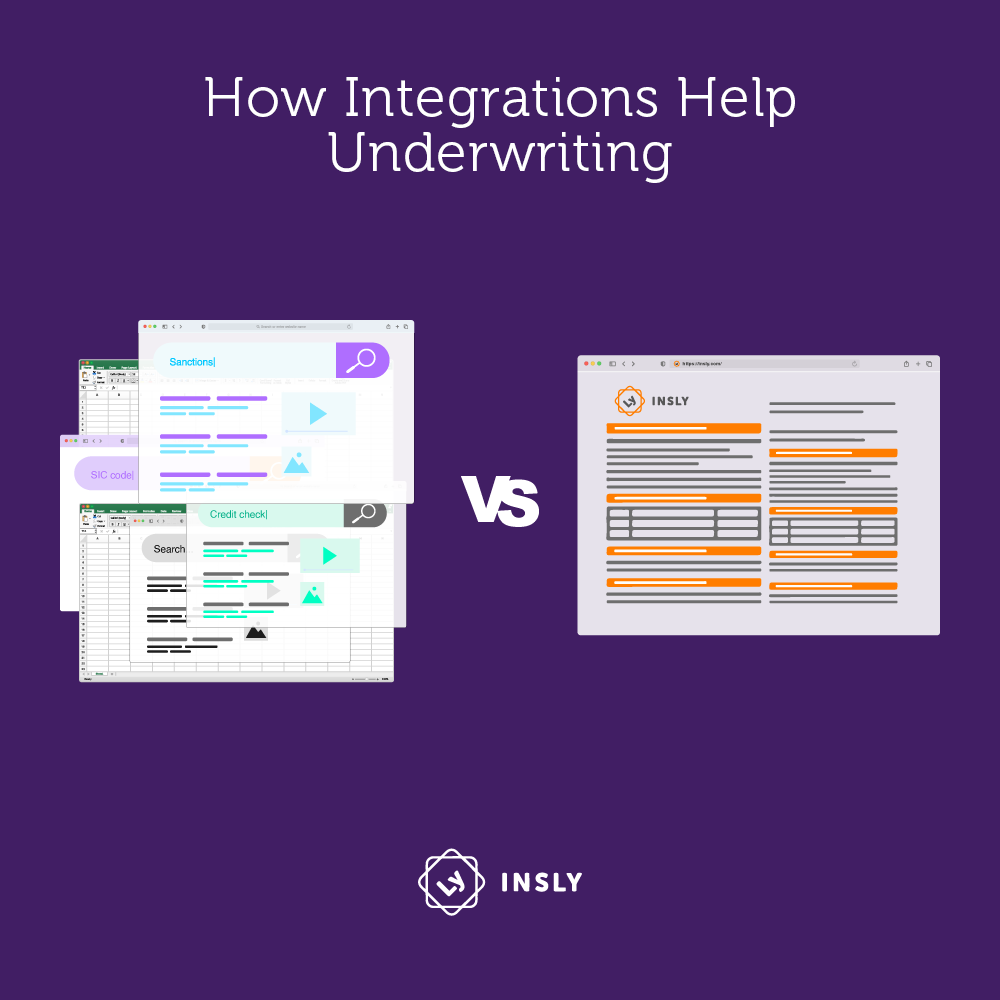

There are several ways that underwriters can be more productive and efficient in their roles. One way is to use advanced analytics and modelling techniques to better understand and assess risk. By using data and analytics to identify key risk factors and predict future outcomes, underwriters can make more informed decisions about whether or not to offer coverage and at what terms.

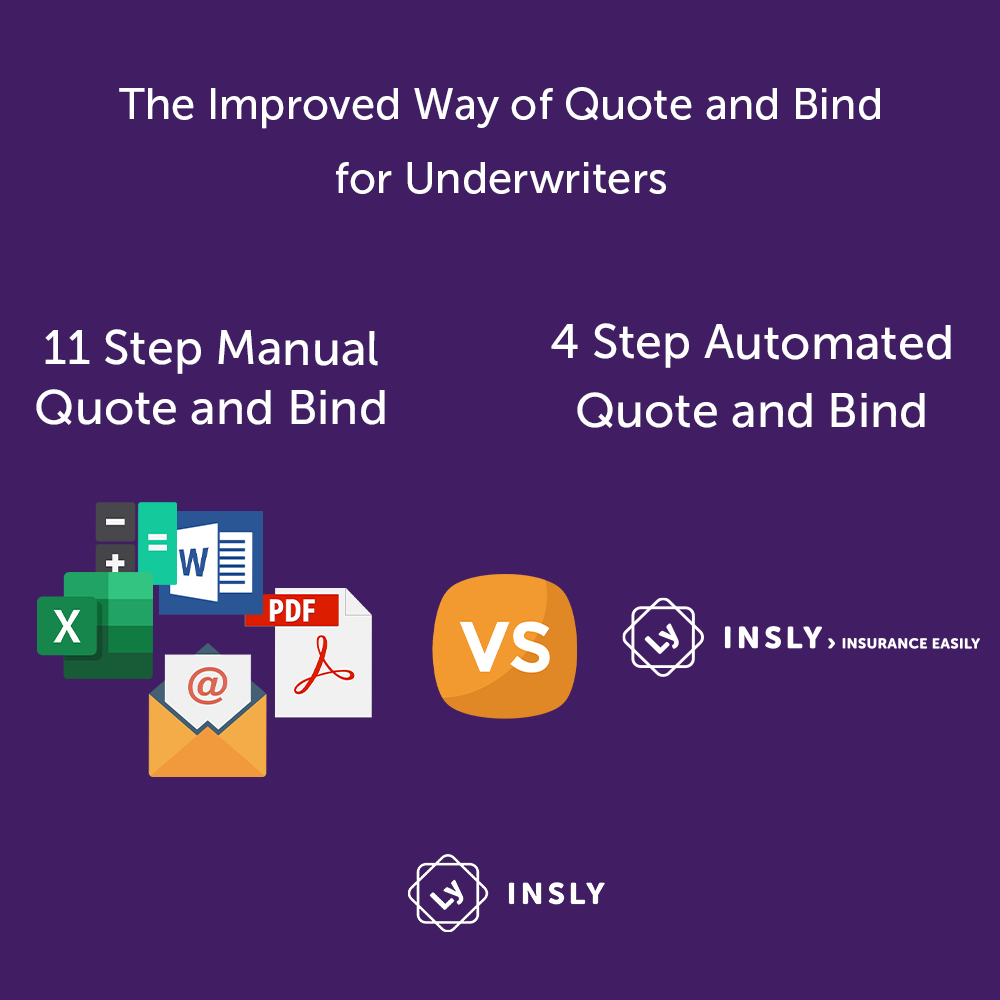

Another way to increase productivity is to use insurance software to automate tasks and streamline processes. Insurance software can provide tools for collecting and analysing data, automating tasks such as policy issuance and claims processing, and providing real-time updates and alerts.

There are several types of tools that underwriters may use to help them be more productive, including:

Insurance software can be a valuable tool for underwriters, as it can help them automate tasks and streamline processes, improve efficiency and accuracy, and better manage customer relationships. By using insurance software, underwriters can more easily gather and analyse data, automate tasks such as policy issuance and claims processing, and provide real-time updates and alerts. This can help underwriters be more productive and efficient in their roles, and ultimately help insurance companies and other organisations reduce costs and increase profitability.